Crucial Mortgage Questions You Need to Asking Your Real Estate Agent

Mortgages are probably the most crucial piece to buying, selling, or just plain owning a home. And, honestly, they are not as hard to understand as you might think. You can benefit from the experience of others who have mortgages (which is just about everybody you know), and with a little homework, you can make the best financial decisions according to the Local Records Office.

What is a Mortgage?

It’s pretty simple: A mortgage is a loan, with your house and land used as security; if you don’t pay back the loan, the lender forecloses on your home. The loan is secured by a lien (the “mortgage”) against the property (your house and land). The lender doesn’t own the house, you do. They just have the lien with your house as their collateral (i.e., the security).

When you are looking for a first mortgage, there are two things to think about: what you can actually afford, and what you can borrow. Why are they different? Because the lender is not going to look at how much you spend in a month on gourmet wine or movies, or how comfortable you’ll be with a big payment. They may be willing to loan you much more than you think you can spend on your mortgage. Only you know how much flexibility or not that your lifestyle has, which determines how much you can afford in a home.

A lender looks at your income (and income potential) vs. your debt, as well as your savings and credit history. Then they determine how big a risk you’d be for the lender to take on. They’re also going to look at the value of the house you want to buy, and the interest rate of the loan you’ll be getting. And then they arrive at a loan amount their firm can live with. In a perfect world, it will match (or exceed) what you need to bridge the gap between your down payment and the price of the house you want.

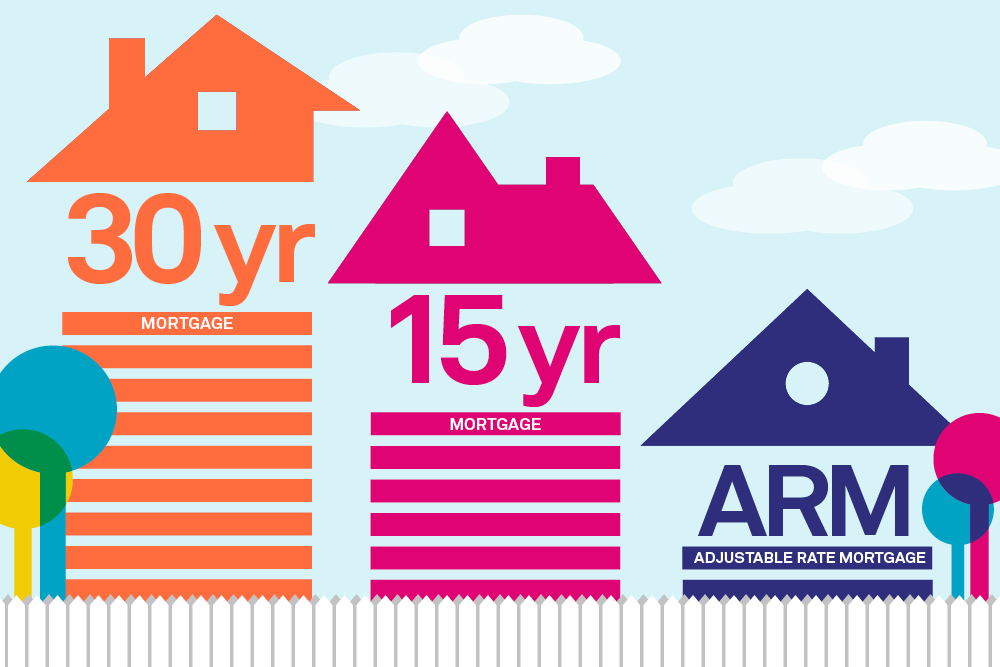

Why are there so many kinds of mortgages! How will I ever figure it out?

When it comes to looking at mortgage types, ask yourself one giant question: What is your goal? Will you be in this new home when the grandkids come to play, or is this a starter home that you’ll trade up in the next five years? The answer to that question will help narrow your mortgage choices.

Why does my length of time in the house matter?

It matters for two reasons: It will determine which type of loan is better for you, and it will dictate whether you look hardest at interest rates or at points.

If you are going to stay in your house and plan to pay off your mortgage over its lifetime, you can get a fixed-rate loan where the payments will not change. (Of course, taxes and insurance are usually included in this type of loan and they might change.) The interest is a little higher than with an Adjustable Rate Mortgage but you have the security of knowing what your loan payments will be.

But if you know you won’t be in the house long, you can get a lower interest rate on an ARM. If rates take a big jump in a few years, it won’t matter because you’re planning on selling them anyway. You’ll also have the option of a hybrid ARM that is fixed for, say, five years, and then adjusts annually.

The lender may charge points (each point is equal to 1% of your home loan amount), and required third parties charge for their services, which increases the cost of the loan. If you sell your home in a few years and have paid points to get a better interest rate, you may not recoup the cost of those fees. And your equity in the house will be minimal, but you are betting the home will appreciate enough to cover the fees, or that the money you save in interest will balance out the additional cost of the loan. (If you stay in the house longer than you expect, you take the risk that you can’t afford the higher payments as the interest rates adjust, or you risk not being able to refinance.)

There’s no free lunch: You can choose between higher rates with no points or lower points, or lower rates with higher points. The key is to compare different types of loans to see what works for your needs.

Tip: In general, you should never pay more than 1 to 1-1/2 points to a lender, depending on the loan. (In certain circumstances, you might pay 2 percent, but only if there is a good reason (e.g., bad credit, complex loan, or you are buying a great interest rate.) You should discuss with an independent mortgage professional the effect discount point have on your rate.

Where can I find today’s rates?

Why are some rates shown as a percentage and as an APR too?

It is a true measure of what you are paying per year against your loan. A loan has a life — whether it’s 15, 30, or even 50 years. You pay in installments, and the principal decreases until the loan is paid off by the end of the term. The payments are evenly spread over the life of the loan, with the interest payments making up the majority of the payment at the beginning, and then the principal paid off toward the end of the term. Pay attention to the amortization schedule, which shows the payments for the life of the loan including interest.

Tip: Pay half your house payment every two weeks instead of one monthly payment. This results in 26 payments per year, one more payment annually than if you just paid monthly. The re-amortized loan will eventually result in more of the payment paid on principal and less on interest. The extra payments go to pay down the principal on the loan.

What else should I watch out for?

Prepayment penalties. Think it’s a good thing to pay off a loan? Well, it might be, but certain lenders charge a penalty if you do. Penalties apply for a specific period of time, usually, 1, 2, or 3 years after the loan is originated. How much is the penalty? Could be six months of interest or 2 percent of the principal remaining on the loan, but it varies.

You might think that it’s stupid to get a loan with a prepayment penalty, but some lenders offer very low (and therefore tempting) interest rates in exchange. Also, some borrowers agree to loans with penalties if they have bad credit and it’s the only way they can get the loan. Mostly, a prepayment penalty is a financial decision. There are situations where accepting a prepayment penalty on a loan can save you thousands of dollars in interest.

What’s mortgage insurance? Do I need it?

If you are making a down payment on our home of less than 20 percent, you will most likely have to get Private Mortgage Insurance (or PMI). It ensures that the lender is guaranteed, by the mortgage insurer, 80 percent of the loan if you default. The insurance premium amount varies by the loan to the value of the house and type of loan.

Government loan programs, such as FHA or VA loans, are backed by the government rather than PMI. There is no monthly mortgage insurance on VA loans, however, you will have monthly mortgage insurance on a new FHA loan.